OPPORTUNITIES ARE ABOUND

The Economy

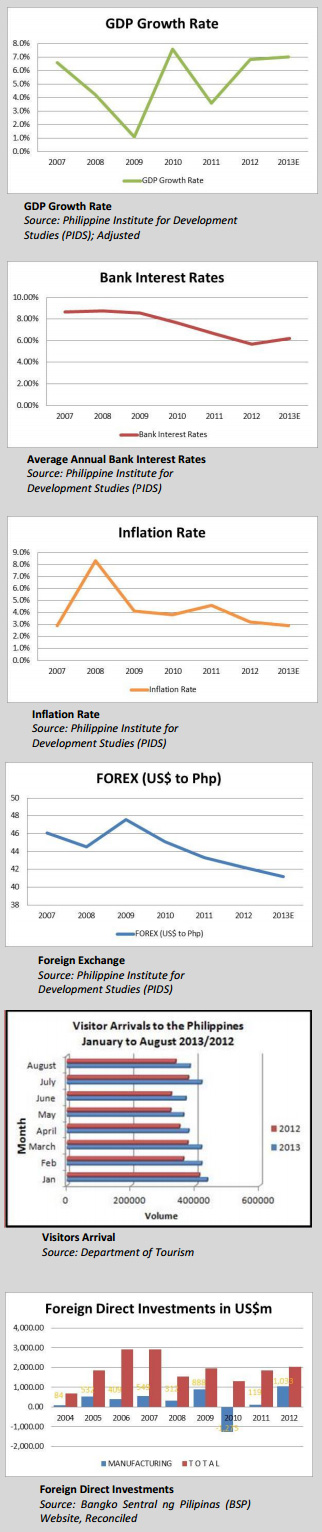

Buoyed by the stable Aquino Administration and its platform for good governance, the Philippines

posted a real Gross Domestic Product (GDP) growth rate of 6.8% in 2012. The recent credit rating

upgrade by Moody’s Investor Services to investment grade (Baa3) reinforces the earlier upgrades from

Fitch’s and S&P’s ratings. While the projected GDP growth rate for 2013 was initially pegged at 7.8%,

this will be adjusted due to the devastations caused by Typhoon Yolanda. Based on initial estimates, the

annualized GDP growth rate will still be in the high 6% hovering to 7%. The average GDP growth rate for

most of the Association of Southeast Asian Nations (ASEAN) for last year, and the projected GDP growth

for this year is 6%. Thus, even with the negative impacts of Typhoon Yolanda, the Philippines is still at

par with or even has a slightly higher growth rate than most ASEAN countries.

The average annual bank interest rate is a very good indicator of stability of available capital, as well as

business sentiment. In the past five years, the single-digit interest rate regime has been experienced.

Starting with high 8% from 2007 to 2009, it has been dipping to 6% since 2011 up to the present.

Likewise, inflation rate is another good gauge of business activities. While inflation rate spiked to over

8% in 2008, since 2009, inflation rate has been averaging 4% and is projected to dip to 3% this year.

The Philippine Peso to US Dollar exchange is a popular indicator of economic health given that the

Philippines is strongly tied to the US economy, and most imports and exports are done with US Dollars.

The exchange has been generally stable with a slight bias to a stronger Peso, presumably due to the

lingering weakness of the US economy in recent years. Moreover, dollar has been steadily generated

from business process outsourcing and stable overseas Filipino remittances. As of September 2013,

total remittances reached US$16.48 billion, which is 5.84% higher for the same period last year.

The total Visitor Arrivals by August of this year breached the

three million-mark, at 3,180,903, which is 11.28% higher for

the same period last year. The 3.18 million arrivals is also

another record as it is the first time that visitor arrivals

reached the three million mark in the month of August.

More importantly, the Philippine Economic Zone Authority

(PEZA) investments from January to October this year

increased by 38.5% (year-on-year), and reached Php 150.91

billion. This is a testament to the increasing attractiveness of

the Philippines given that the total foreign direct investments

in 2012 grew by 42.68%.

All of these key indicators translate to robust economic

fundamentals and sound investment environment. In turn, the

macroeconomics fuels the strong demand for the different

sectors in the property market.

Office Market

The demand for office spaces in Metro Manila is still very

robust, with occupancy rates ranging from 94% to 98% in the

different business districts. The BPOs’ continued expansion

represents the biggest demand driver. Developers are pushing

ahead with their projects to capture this pent-up demand.

Rents have been inching up, even with new buildings coming

online, due to the tight supply. Thus, the market has been seeing pre-leasing again especially from big occupiers to avoid

the space crunch. While Ortigas, Alabang and Quezon City

offer alternative sites, Makati CBD and BGC remain as the

preferred office locations.

Since Makati remains the location of headquarters of major

companies and global businesses, developers and investors

have been looking for old buildings that can be renovated or

re-developed. Some big companies even acquired existing

buildings that can be converted for their own use and

occupancy. While rental rates are increasing due to space

limitations, these are still within tolerable limits. Rents in

Premium Grade A are still slightly higher than Php 1,000 per

sqm per month, while rents in Grade A have an average of Php

750 per sqm per month. Small and old buildings in Makati are

offering rents at an average of Php 550 per sqm per month.

The very strong demand for Fort Bonifacio Global City (BGC)

lots has pushed accommodation values even higher than in

Makati land values, since most lots in BGC are below the 16-

floor area ratio (FAR). BGC is indeed the preferred location of

BPOs. The interest in BGC’s office market has further

thickened with the recent acquisition of five buildings of the

Net Group by no other than SM Group, at an estimated tag

price of Php 18 billion. Meanwhile, asking prices in BGC are

way above the Php 30,000 accommodation value. The cross

section at BGC, however, does not directly compete with

Makati CBD. Makati still caters to the corporates and

traditional offices, while BGC buildings (green and all) mainly

cater to BPOs. BGC and Makati are actually complementing

one another, which is a welcome decongestion of Makati CBD.

Residential Market

While various developers have been more discerning with

their project launches, the residential market continues to be

very active. The high-end segment remains to be strong and

top brands of the Ayala, Century Properties, Filinvest,

Robinsons, and Rockwell Groups have been introducing

products catering to the rich and famous. It is no wonder that rents in luxury high-end condo units are

well above Php 200,000 per month,

depending on the floor areas. Rents in the

villages, given the very limited supply,

remain to be strong ranging from Php

300,000 to Php 500,0000 per month.

For the mid-market and affordable

segments, the prevailing low interest rates

and high liquidity allow both developers and

buyers access to various financing schemes.

Various developers continue to tap the

availability of financing from the banks and

even from international players. These

financing institutions assure them access for

land banking as well as to complete their

ongoing residential projects. This highly

liquid regime likewise gives their projects a

better likelihood of being sold as this would

open their units for sale to a larger market,

locally and internationally.

Retail Market

The Filipinos’ affinity to malls and their propensity to spend have been keeping the retail owners with

enviable cash liquidity. Retail owners have been raking in from overseas Filipinos and their families, and

from the ever-increasing number of BPO employees. Even for self-employed or small businessmen, or

the traditional employees, disposable incomes continue to rise over time and these incomes funnel to

the malls. With a lot of office and residential developments, various retail platforms have been

introduced as well, such as the mini-grocery and convenience store setups. Some developers have

either setup their own retail division or forged alliance with well-known retailers.

Retail malls are still controlled by a few big players. Recently, ownership or strategic alliances have been

shifting, mainly brought about by the strategic plays of the key players. Early this year, the SM and

Walterwart Groups structured a joint venture to counter the aggressive moves of Puregold Price Club

Inc., which includes S&R Membership Shopping. Puregold, apart from its recent fray in the Philippine

Stock Market, also acquired four operating Eunilaine foodmarts and its 11 operating “Grocer E

supermarts”. Other strategic retailers are the Araneta, Ayala, Federal, Filinvest, Greenfield, Kuok,

Metro-Gaisano, Ortigas, Robinsons, Rockwell, Sta. Lucia, and Star Groups.

Successful retailers have been dictating lease rates, terms and

conditions of occupancy, delivery, and even control the supply

chain, thereby, putting pressure on the suppliers to lower cost. As

in the previous years, retail malls have been generating one of

the highest, if not the highest yields, in the property sector. It is

projected that further consolidation shall happen in major retail

platforms, and niche players would continue to look for untapped

platforms in specialized markets.

Hotel and Gaming Market

The hotel market has been benefitting from the steady rise of the

Philippine tourism industry. It is interesting to note the recent

race to put flags in major CBDs, such as the Holiday Inn and

Fairmont in Makati, Grand Hyatt and Shangri-la in BGC; and some

chains like the Ascot Group and the affordable Tunes Hotels have

been busy criss-crossing the CBDs. The biggest driver, however, is

the booming Gaming industry. The success of the Resorts World

Manila (Megaworld Group) and Solaire Manila (Bloombery

Resorts) had reverberated to the big players. Large-scale projects

are now underway mainly in the “Bay Area” and airport area.

Given the requirement of the Philippine Amusement and Gaming

Corporation (PAGCOR) to put up hotel rooms in exchange of

gaming licenses, a lot of quality supply of hotel rooms would be

sprouting.

On the demand side, record-breaking tourist arrivals have been

happening almost every year. For 2013, it is the first time that the

3 million-barrier, a pipe-dream a decade ago, was breached as

early as the month of August. More importantly, the Department

of Tourism has been lining up major international and interregional events for the Philippines, such as hosting the Asia-Pacific Economic Cooperation Summit in 2015. Bilateral (e.g.

Philippine-Brazil no-VISA travel) and multilateral (e.g. ASEAN

integration) arrangements would further boost the influx of

tourist in the Philippines.

Industrial Market

The Philippine Economic Zone Authority has been harping that

vacancies in PEZA parks have been declining and there have been steady inquiries on the Philippine industrial market. While one

has to take this with a grain of salt, the bell-weather of industrial

market is the combined market of the Clark Special Economic

Zone (CSEZ) and the Subic Bay Freeport Zone (SBFZ). Officially,

CSEZ has a total area of approximately 29,000 hectares while

SBFZ has a total area of about 67,000 hectares. In terms of real

space for lease, the Clark Development Corporation (CDC) is

leasing a total area of approximately 116 hectares while the Subic

Bay Metropolitan Authority (SBMA) is only leasing a total area of

51 hectares.

In terms of demand, CSEZ has approximately 1,100 locators, and

SBFZ has a total of 600 locators. The success of both Clark and

Subic has been through identifying major tenants that would sublease to smaller tenants. In the case of CSEZ, CDC leased big

spaces to Berthaphil Inc., Global Gateway Development Corp.,

and PhilExcel Business Park Inc. The SMBA leased big areas to the

Japanese-developed Subic Technopark and the Taiwanese-driven

Subic Gateway.

Strategic Opportunities

The Office Sector shall remain a favourite given the very tight

office supply. Developers and landlords should take advantage of

the “pre-leasing” phenomenon to fill up their spaces, and/or fast track their constructions. Yields shall remain strong and could

easily out-pace interest rates. The major decision points are what

market to target (BPOs or traditional companies); what

technology to use (green or traditional building); and what

percentage to sell (pre-leasing or pre-selling). The Ayala and

Century Groups have been benefitting from pre-selling of office

spaces.

Commercial spaces offered by the retailers shall continue to

enjoy the highest yields. Retail malls have been expanding their

tenant-mixes that include major government offices and

collection agencies to attract more and more foot traffic. The

general concept is to attract shoppers in the mall and keep them

in for as long as possible by offering various services and products. For niche players, they should consider

location-specific opportunities, especially for smart

shoppers that avoid long queues and tight parking in

malls, and prefer relaxed shopping and dining.

The Residential Sector is highly opportunistic. Luxury

residential development is always resilient but more

expensive to build. Mid-market is very competitive and

location-specific. Demand for affordable and socialized

housing has been north of three million, but the

marketing is based on volume and highly supported by a

number of government agencies, and the margin per

unit is relatively lower. The common trend is mixing

residential with office and retail developments. More

importantly, it is instructive to conduct accurate market

scanning on the sizes, amenities and pricing of the

residential products to be offered; and how much retail

and office spaces to be blended in the mix.

The Hotel Sector has always been a boom-time play.

With the investment grade status of the Philippines and

record tourist arrivals, this is the best time to put up

hotels. The key questions are what “star” to put up

(which is location-specific); would it be owner-operated

or managed by well-known brands; and would the hotel

development co-locate with the casinos or traditional

tourism areas.

The Industrial Sector has been the laggard of the

Property Market for more than a decade. In recent

years, foreign companies have been steadily coming back to the Philippines. The years 2012 and 2013

showed faster growth of foreign direct investments. There are now a number of applications to get

PEZA accreditation for a number of economic zones all over the Philippines.

The Philippines is in a very good position to sustain the upbeat Property Market. Even with the

destruction caused by Yolanda, most players seeing the opportunities after the crisis. The Philippine

government, together with various local and international groups, has generated billions of Pesos for

rehabilitation and reconstruction. All sectors are now indeed growth areas, with some caveats in the

residential and retail segments. Great opportunities are abound, and are supported by real demand,

strong economy, and positive business climate.