SPOTTING MARKET GAPS

The Economy

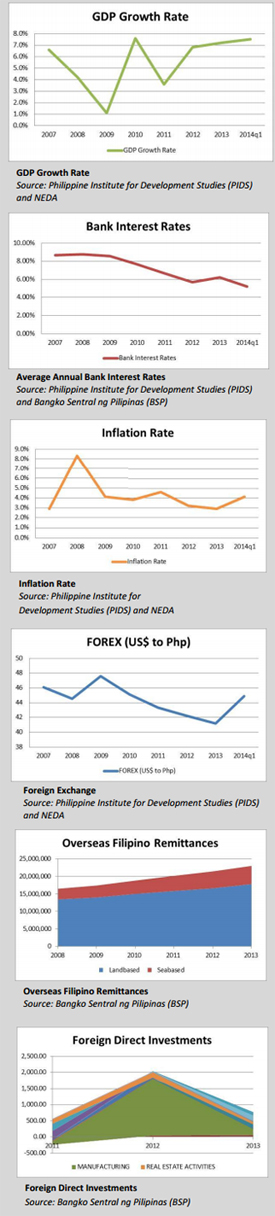

Philippines’ full year target for 2014 is between 6.5-7.5% growth, on the back of the 7.2% real Gross

Domestic Product (GDP) growth in 2013 even with the impact of the natural disasters, according to

National Economic and Development Authority (NEDA). The International Monetary Fund (IMF) pegged

the average GDP growth rate for most of the members of the Association of Southeast Asian Nations

(ASEAN) at 5.1% this year, which is lower than the Philippines’ target. The IMF projected the world’s

growth at 3.1% for 2014.

Based on Bangko Sentral ng Pilipinas (BSP) statistics, the average bank interest rate continues to dip at

5.19% as of February of this year compared to 6.21% by the end of 2013. Inflation rate by February is

4.1% compared to 2.9% by end 2013. Given the brisk economic activities, especially in manufacturing

and real estate, the BSP recently increased the reserve requirement ratio by 1 percentage to 8% across

all banks. This move has been expected to avoid overheating of the economy and to curb speculation,

especially in the real estate market.

The Philippine Peso to US Dollar exchange shows a stronger dollar from Php 41.2 by end 2013 to Php

44.9 by end March 2014. This indicates that the US economy has been steadily improving since dollar

remittances from overseas Filipinos have been stable and reached US$22.97 billion by end of 2013. For

January of this year, overseas Filipino remittances total to US$1.80 billion compared to US$1.70 billion

for the same period last year.

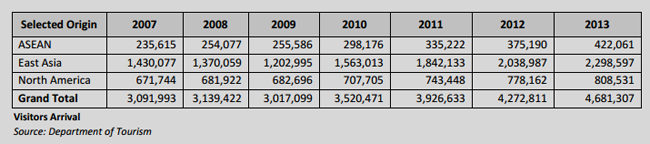

The total Visitor Arrivals last year was a record breaking 4.68 million, which is 9.56% higher than 2012.

Visitor Arrivals in January of this year increased by 5.8% to 461,363 from 436,079 in the same month

last year. The government is targeting a total Visitor Arrivals of six million this year.

Foreign direct investment (FDI) has been dominated by

manufacturing investments and real estate activities,

outside of debt instruments and reinvested earnings.

Manufacturing comprised 51% of the total foreign direct

investments in 2012 and 33% in 2013. Real estate activities

account for 8.2% in 2012 and 10.6% in 2013.

These key economic statistics indicate a sustained economic

growth and sound investment environment for 2014. All

indicators point to another banner year for the real estate

industry. While some quarters are getting uncomfortable

with the very active industry, even prompting the BSP to

increase reserves, thereby withholding approximately Php

60 billion to the financial market, the real estate market is

basically becoming more competitive. This is an excellent

prelude to prepare the industry with the upcoming ASEAN

integration by 2015.

Most people would prefer a competitive market. This would

reduce inefficiencies and would promote good product and

pricing for the consumers. Now more than ever, real estate

players should be able to spot market gaps, ahead of the

other players if possible. Developers cannot anymore rely on

the “build it and they will come” mantra as buyers have

more choices and are more discerning. Misreading the

market would be costly. Diligent players should be patient

and deliberate with their target location, target product,

target market and target timing. Spots of opportunities are

present in the ever-increasing real estate market, whether

redevelopment projects within Metro Manila or green field

developments outside. Within the sectors of the real estate

markets, gaps are still waiting to be serviced. More

importantly, the government has been active in building

crucial infrastructure projects, and in generating tourist

arrivals and investors that would translate to real estate

demands.

Office Market

The Business Process Outsourcing (BPO) industry remains

the driver of the demand for office spaces not only in Metro

Manila but the entire Philippines. After experiencing more

than 20% annual average growth in the past 10 years,

industry estimates point to a slower 15% annual growth

beyond 2016. For 2014 and 2015, the average of 20%

growth is still doable. At present, vacancy of Premium Grade

A and Grade A buildings is at all-time low of below 5% across

the major business districts. Grade B and C buildings may

have higher vacancy levels, but these buildings would

eventually absorb the overspill of demand for office. Some

of these buildings may even be up for redevelopment,

whether into an office, residential or mixed used building.

Big space users have been committing to pre-leasing

agreements to avoid the space crunch. In recent months,

pre-selling of office spaces have been picking up, which used

to be unheard of after the Asian financial crisis in 1997.

Rents in Premium Grade A are higher than Php 1,000 per

sqm per month, while rents in Grade A have an average of

Php 750 per sqm per month. Small and old buildings in

Makati are offering rents at an average of Php 550 per sqm

per month. Depending on the vacancy of the buildings, rents

are projected to increase between 3%-7% this year.

There are a lot of opportunities in the office market.

Developers are now more confident building office buildings

since they can get pre-commitments. Owners of old

buildings may consider capturing the demand by retrofitting

their facilities; or they may consider redeveloping

altogether. Joint developments with building owners, even

with condominium corporations, are becoming common

especially when they don’t want to sell the land or would

want to share on the upside of the development. For

straight-forward office projects, developers may opt to sell

to recoup their investment faster, or may choose the

recurring income. In most cases, developers would want to find the balance between selling some floors

and retaining some floors for leasing; except for Zuellig Building which is purely for leasing.

Residential Market

The residential market shall continue to be very active given that the demand for housing is

projected at 3.9 million, and possibly reaching 6 million in the next few years without serious intervention. The mid-market has been the center of discussion due to the hyper activity in this segment, and some are even

asking the question of property bubble, especially in Metro Manila.

The Housing and Land Use Regulatory Board (HLURB) and Pinnacle Research statistics show that from

2013 to 2017, there are 301 ongoing condominium projects in Metro Manila totaling to 134,421 units.

The mid-market segment accounts for the largest chunk at 37% or 49,997 units. Studio and one-bedroom units account for 77% or 104,028 units. Assuming that all of these projects are completed on

time, these numbers are still well below the target of one million housing units by 2016 of Subdivision

and Housing Developers Association, Inc. (SHDA) to bridge the gap in housing requirements.

The high-end segment continues to be vibrant, especially with the sales abroad and to foreigners. This

segment is only the active segment in leasing, with rents well above Php 200,000 per month, depending

on the sizes. Rents in the villages generate the highest levels ranging from Php 300,000 to Php 500,000

per month.

The affordable and socialized segments are still underserved. Based on the same database above, only

24,981 units are targeting these two segments in Metro Manila. This is understandable since majority of

the socialized and economic housing projects are located outside Metro Manila to take advantage of

lower land prices.

Retail Market

Developers are relentless in having a piece of the

retail market, exploring various retail platforms,

setting up their own retail brands or forging alliance

with well-known local and international retailers.

DoubleDragon Properties Corp., the group that owns

Jollibee and Mang Inasal among others, intends to put

up 100 CityMalls with an aggregate space of about 1

million sq.m., by 2020. CityMall will be constructing

community centers of 5,000-10,000 sq.m., in sizes

that target to serve the provinces. In a strategic move,

the SM Group bought 34% into CityMall Commercial

Center, Inc., the retail company of the DoubleDragon

Group.

The SM Group is pursuing expansion this year with 20

supermarkets and three shopping malls. Robinsons

Group recently opened two full service malls, the

Robinsons Place Roxas in Panay Island, and Robinsons Place Santiago in Isabela, expanding to a total of

37 shopping centers nationwide. Its Ministop operations, a franchise of the Japanese brand, target to

reach over 500 stores by yearend.

Rustan’s Supercenters Inc. is expanding its operations by adding 13 more branches by the end of 2014.

The Ayala Group has been busy introducing its new mall brand “District” in Imus and Dasmariñas,

Cavite, and in Bacolod. Filinvest Group’s Festival Supermall started its four-level mall expansion with

“River Park” that would feature foreign fashion brands. The Century Property Group recently opened its

Century City Mall in Makati.

Super 8 Retail Systems is investing about Php 1.5 billion to hit a total of 75 stores within the next three

years. It also acquired America’s leading convenience store “Circle K” to add to the group’s retail

platform in servicing the consumer goods market in the country.

Major retailers shall continue enjoying high lease rates and occupancy levels. Malls are expected to

generate the highest yields in the real estate market. It is projected that more innovations in retail

platforms by both retailers and niche players would continue to service the untapped segments in the

market that would reach to the most number of Filipino shoppers.

Hotel and Gaming Market

Last year was a banner year for Visitor Arrivals reaching 4.68M. January data shows it is higher than the

arrivals for the same month last year. The hotel market shall continue to benefit from the steady rise of

the Philippine tourism industry and the ASEAN integration. In addition, the government signed an

additional air-link agreement with Japan that would increase weekly flights from 119 to 400. The

Department of Tourism (DOT) is projecting an increase of 15%-20% of Japanese travelers coming in. Last

year, a total of 433,705 Japanese visited the Philippines.

In terms of room rates, five star hotels are charging north of US$ 300 per night on the average. Four star

hotels have breached the US$ 250 rate on the average. Existing hotels have been enjoying increasing

rates due to record-breaking tourist arrivals.

On the supply side, about 4,000 rooms are targeted to be completed this year. The major chunk would

be in the PAGCOR Entertainment City area, such as Belle Grand City of Dreams (920 rooms), Radisson

Hotel (500 rooms) and Tune Hotel (204 rooms).

The Robinsons Group aims to complete 1,200 rooms in its portfolio this year with three Go Hotels

located in Ortigas Center, Butuan and Iloilo. In addition, the Group also signed with Singapore-based

Vanguard Hotels Pte. Ltd. and Roxaco Land Corp. to construct at least five Go Hotels in the next two

years.

The Ayala Group has launched two new Seda hotels in its emerging mixed-use developments in Vertis

North and Circuit Makati, and may take three years to complete.

Shanghai-based Jin Jiang International Hotels is putting its flag in Makati (70 rooms) and Ortigas Center

(95 rooms). Jin Jiang Inn Greenbelt and Jin Jiang Inn Ortigas are targeted for completion this year. More

and more international hotel operators are expanding their brands in the Philippines like Ascott, Conrad

Hotels and Resorts, Crowne Plaza, Dusit Thani, Fairmont, Hyatt, Holiday Inn, Intercontinental, Mandarin,

Marco Polo Hotels, Marriot, Maxims, Oakwood, Peninsula, Radisson, Renaissance, Shangri-La Hotels and

Resorts, Sheraton Hotels and Resorts, and Solaire Resort and Casino.

Industrial Market

The manufacturing sector continues to generate a significant chunk of foreign direct investments. For

2013, manufacturing accounts for US$216.41 million, second only to the new category of “Water

Supply; Sewerage, Waste Management and Remediation Activities” that accounts for US$ 461.38

million. This is one of the reasons why the growth of the manufacturing sector reached 12.3% in the

fourth quarter of 2013, making it the fastest growing industry in the Philippines during the quarter, and third overall for 2013. Manufacturing sector’s full year growth of 10.5% is nearly double the 2012

growth of 5.4%.

The Philippine Economic Zone Authority continues to promote the establishment of economic zones

due to decreasing vacancies in existing PEZA site. The combined available industrial space in Clark

Special Economic Zone (CLARK) and the Subic Bay Freeport Zone (SUBIC) is at a historic low of 150

hectares. CLARK has been filled up by 1,100 locators while SUBIC has a total of 600 locators.

Another sign of a healthier manufacturing sector is the recent purchase by Mitsubishi Motors

Philippines Corp. (Mitsubishi) of the 21-hectare non-operational manufacturing plant in Sta. Rosa,

Laguna. Mitsubishi is committed in expanding its sales and production capacity which is part of its new

stage of growth mid-term plan until the end of 2016 fiscal year.

OPPORTUNITIES IN MARKET GAPS

The office market remains to be a favorite given the high occupancy rate and an average yield of 10%.

Developers and landlords should take advantage of pre-leasing and pre-selling. Owners of old buildings

would have to decide sooner or later if they want to retrofit their buildings to capture the pent-up

demand for office, or redevelop their buildings altogether.

Commercial spaces in retail malls shall continue to generate the highest yields to the big retail owners.

For niche players, they should consider location-specific opportunities, especially for smart shoppers

that avoid long queues and tight parking in malls, and prefer relaxed shopping and dining.

The residential sector is a very big market. Luxury segment on one end and the affordable and socialized

housing on the other end remain to be underserved. Luxury is typically more expensive to build but the

margins are higher. Socialized and economic housing projects have lower margins on per unit basis, but

developers may get a number of fiscal and non-fiscal incentives that would push profitability higher.

Mid-market is very competitive and location-specific. This is the segment where due diligence would

pay off in terms of market scanning the sizes, amenities and prices of the residential products to be

offered; and perhaps, how much retail and office spaces to be blended in the mix. The leasing out of

mid-market residential is another gap in the market that may need to be served soon.

The hotel sector is riding on the investment grade status of the Philippines and record tourist arrivals.

The ASEAN integration and the increased in air-link with Japan would further boost the total number of

visitors. Finding the right location, the right size, right brand are some of the key questions for

developers.

The industrial sector is in a stable growth as more and more foreign companies and investors have been

coming back to the Philippines. Applications to get PEZA accreditation to locate in economic zones and

even to build new ecozones are on the rise as well.

The Philippines is poised to sustain the growth in the real estate market. All of the sectors are on

expansion mode due to real demand, liquid financial market and strong economy. Positive business

climate and servicing the market gaps would likely be a continuous boon to diligent actors in the

property market.

Download the PDF Version